How to Estimate Retirement Spending

- Financial PlanningHow much will I need each month to cover my expenses during retirement?

If you want to feel comfortable stopping your “regular” work, you’ll need to answer this fundamental financial life planning question. But as I’ve said many times before, no one really “retires” anymore in the sense of stopping all activity and never leaving the house again. Many of us will even continue to work for money, but what we’re talking about here is stepping out of the high-pressure, high-time-commitment phase of working into a kinder, gentler phase. I’ll just use the word “retirement” here because it’s shorter than all of that.

It seems so complicated to figure out how much money you’ll need during that retirement phase. There are online calculators with 3,000 inputs, and you need to build them from the ground up, track them over time, and…I’ve already lost you. This is why financial life planning is an occupation. But isn’t there a quicker and easier way to estimate your expenses during retirement? Yes, Virginia, there is.

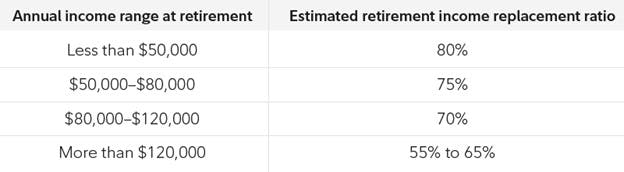

Let’s start with an estimate of 80% of your pre-retirement spending. This is the estimate I see most commonly, and it’s a fine place to start for most people. As it turns out, the more you’re making when you retire, the lower that replacement ratio will need to be. Fidelity provides the following estimates of the percentage of your pre-retirement income you’ll need to replace. But if you will be making $300k or more when you retire, please see a financial life planner, because these Fidelity models don’t have enough data in your income range to make a good stab at it.

OK, now you have a place to start. What else should you consider when estimating how much you’ll spend each month during retirement?

1. Housing: Will your house be paid off when you retire? Will you stay where you are now or move somewhere less expensive? More expensive? Will your plans change based on other factors, like kids moving out or grandchildren being born? Update your baseline retirement budget based on your housing plans.

2. Other obligations: Will you be paying for someone to go to college even after you retire? Will you have people who will depend on you for care? Save for that now, if you can, or add it to your retirement budget. If you have aging parents, make sure they have planned for long-term care expenses and other health-related issues, or put some extra in your budget for that as you’re able.

3. Lifestyle: What do you plan to do when you retire? Are you a big traveler, or do you prefer to stay at home? Add 6% or more to your baseline budget if you want an active early retirement. Do you have expensive hobbies or things you want to buy? Don’t forget to add those. Also keep in mind that everyone slows down over time, even those of us who are vigorous and healthy now. When you’re 80, you may not want to take the speedboat out or fly to Taiwan. You can step your budget down over time to account for this.

4. Health: How IS your health? How much will health insurance cost if you retire before Medicare age? Do you have long-term care coverage? If you don’t, get it if you are healthy enough to qualify. Genworth estimates (as of 2023) that the average monthly cost in the US for in-home home maker services was $5,720, and the average for assisted living was $5,350. In a nursing home, monthly costs started at $8,669. My friends, note that these are US averages! Where I live, it’s a lot more expensive than the average. How about you?

5. Taxes: Make sure you know which of your retirement income sources are taxable, so you’ll know whether that income covers your expenses. For example, the income from retirement accounts like 401(k)s, 403(b)s, IRAs, and pensions is taxable. You’ve already paid taxes on your Roth IRA money as it went into the account, so those funds aren’t taxable when you take them out. For Social Security, the amount of tax you’ll pay depends on your Adjusted Gross Income, but you’ll never have to pay tax on more than 85% of your Social Security check.

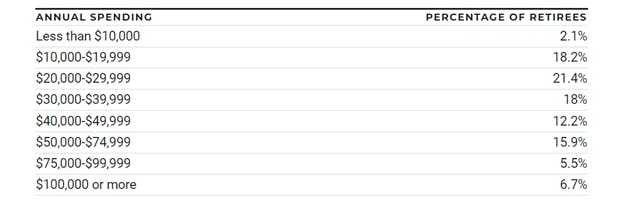

That’s all great, you may be thinking, but am I even in the ballpark? Well, the US Bureau of Labor Statistics tells us that in 2022, households led by someone who was 65 or older spent an average of $57,818. “$57,818 a year?” I asked myself incredulously. “That won’t even keep me in stockings and fans!” Yes, it’s VERY expensive where I live, as I may have mentioned a few hundred times, so take this average with a grain of salt based on where you live.

In 2020, the BLS also broke down the average to show what percentage of retirees fell into various levels of spending. For your delectation:

A final word: Please recognize that you WILL need to adjust your spending plan along the way. That’s the inevitability of life; you never know what might happen down the road, and that’s OK. You set up an emergency fund, insurance, and all the other ways of protecting yourself as best you can. If you need to, you can spend less for a year or two, or move to a less expensive area or make other changes.

Now, I highly recommend you hire a financial life planner to do all of these calculations for you, plus all the other great things planners do, like convincing you to get life insurance and do your estate planning and following up until you do it all. But if you’re looking for a general idea of how much you need to save or when you might be able to retire, this is a good start. Happy navigating!